Flash News

Flash News

The two football giants on the field, Brazil and Germany, are looking for a ticket to the 1/8th.

Avoid peak hours, temperatures reach up to 39 degrees today

Rama retracts statement: I did not say "F*ck you" to Albanians

'Albanian Files' exposes Rama, Berisha: I invite Eurojust and Europol to investigate 523 projects

Marjana Koçeku warns of more departures from the Socialist Party: Parliament seals the party's decisions

Albania as the "black sheep", banking groups have lower returns compared to their average

Politiko

2026-06-29 11:03:40

Foreign banking groups appear dissatisfied with the profitability of their business in Albania. According to a survey conducted by the European Investment Bank (EIB), most foreign banking groups report lower than average profitability from their activity in Albania.

Although the performance of the banking market has improved in recent years, profitability indicators remain at levels that are not fully satisfactory for their shareholders. In particular, the strong increase in capital requirements by the Bank of Albania has resulted in lower returns on capital compared to most other markets in the Region.

Albania appears as the only market in Central and Southeastern Europe where returns on equity for banking groups are lower than average levels at the group level.

Also, according to a survey of banking groups, Albania is one of the markets with the lowest potential, at levels comparable to Serbia and Bulgaria.

These results indicate that Albania may still be an unattractive market for new investments from large banking groups.

Albania seems to be an exception compared to other Central and Southeastern European markets.

According to the survey, international banking groups see this area as a market where they intend to grow further in the long term. Three-quarters of banking groups operating in these regions plan to expand, while none intend to reduce their presence.

Most parent banks in Central, Eastern and Southeastern Europe have either maintained or increased their exposure to the region over the past six months. Looking at their long-term strategies, parent banks continue to favor expansion.

However, the banking groups in question assess the market potential as particularly high in the Czech Republic, Romania and Slovakia, while seeing this potential as more moderate in the Western Balkans.

They also report higher profitability in the region compared to the group's overall operations, particularly for Bosnia and Herzegovina, Bulgaria, the Czech Republic, Hungary, Kosovo, North Macedonia and Serbia.

According to the survey, credit demand is expected to remain strong in the region, while credit conditions are expected to ease slightly in the coming months. In the second half of the year, credit demand is expected to remain strong for businesses and households.

Demand for credit has remained strong in recent years, driven mainly by individual customers.

In contrast, credit supply in the region has been weaker, despite some signs of improvement in 2024, and has remained broadly stable over the past two years.

Access to funding for local branches remains favorable and has improved over the past six months, supported by higher retail and corporate deposits.

In recent years, the markets of Central and Southeastern Europe have been regaining attention from major European banking groups. After an exit process of many important players following the 2008 crisis, it seems that the consolidation and improvement of the banking market in these countries is gradually making them attractive again. Most banking groups are trying to return to organic growth, but in the meantime they are also showing interest in new acquisitions, with the aim of increasing their market share and efficiency./ Monitor

Latest news

Belgian newspaper: Protests exposed Rama's image as a gangster

2026-06-29 12:14:00

Scotland coach resigns after World Cup exit

2026-06-29 11:36:35

Police officer dies in Vërmica, suspected of being hit by a driver from Albania

2026-06-29 10:05:08

"Banjat e Benja between Harese and the destruction of Albanian nature"

2026-06-29 09:32:24

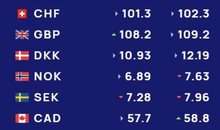

Foreign exchange rate June 29/ How much the dollar and euro are bought and sold

2026-06-29 09:13:34

AP dedicates report to protest: "Flamingo Revolution" draws world attention

2026-06-29 08:56:11

Avoid peak hours, temperatures reach up to 39 degrees today

2026-06-29 08:19:42

Morning Post/ In 2 lines: What mattered yesterday in Albania

2026-06-29 08:02:17

Over 1,300 dead from heatwave in Europe

2026-06-28 21:57:50

Mrekulli në Venezuelë! Foshnja 18-ditëshe shpëtohet pas 32 orësh nën gërmadha

2026-06-28 21:11:49

State capture through territory

2026-06-28 20:56:31

Ronaldinho returns to the field after 11 years

2026-06-28 20:43:17

Why do we cry when we are happy? Science gives the answer

2026-06-28 20:20:29

29th protest in Tirana, citizens march towards the Prime Minister's Office

2026-06-28 19:38:10

WHO warns: Europe is experiencing one of the deadliest heatwaves

2026-06-28 18:33:01

"The Albanian Files": How did Albania turn into a money laundering laboratory?

2026-06-28 18:14:59

Before the EU, 20% of construction sites lack safety standards

2026-06-28 17:58:11

Publikohet formacioni më i mirë i raundit të tretë në Botëror

2026-06-28 17:35:31

Si të mbroheni nga vala e të nxehtit?

2026-06-28 17:12:55

Berisha heads to Vienna for the EPP Assembly, focusing on the report on Albania

2026-06-28 16:49:42

Why don't Germans have air conditioning at home?

2026-06-28 16:30:40

Fire in Mallakastër, Bylis Archaeological Park at risk

2026-06-28 16:10:22

Conflict with brothers over properties, former director of Vlora Police arrested

2026-06-28 15:53:52

Rama retracts statement: I did not say "F*ck you" to Albanians

2026-06-28 15:39:23

Chain accident on the Durrës-Tirana highway, two injured

2026-06-28 15:20:25

EU grants $5.6 million in aid to Venezuela after devastating earthquakes

2026-06-28 13:22:38

Citizen "nails" Shalsi: Nikaj-Mërturi has not seen any investment from you

2026-06-28 11:19:40

62-year-old prisoner dies after being in the same cell with his son

2026-06-28 11:01:53

Albania, bonus-malus in "miniature", how do we compare with Europe

2026-06-28 10:24:39

Agricultural waste, untapped potential for the circular economy in Albania

2026-06-28 09:44:41

Tourist Albania "stuck" in traffic

2026-06-28 09:00:18

Horoscope, discover the star forecast for your sign

2026-06-28 08:40:31

Weather forecast for today, June 28, 2026

2026-06-28 08:18:30

Morning Post/ In 2 lines: What mattered yesterday in Albania

2026-06-28 08:02:47

7 phobias of people you've probably never heard of

2026-06-27 22:00:07

VAR anulon golin e Iranit, publikohen pamjet që ndezin polemika

2026-06-27 21:34:04

Protein discovered that may be linked to brain aging and memory

2026-06-27 20:45:28

Italian MEP joins protest against Rama

2026-06-27 20:18:16

Vučić announces resignation: I will only be in office for a few more weeks

2026-06-27 19:55:13

MEPs join protest in Tirana, revolt against government enters 28th day

2026-06-27 19:15:15

Government repression of protests continues, minister threatens more 'non-grata'

2026-06-27 18:55:00

Video/ Scorching heat in France, citizen fries eggs and bacon on window

2026-06-27 18:18:29

Germany hit by record temperatures

2026-06-27 18:01:04

Foods to avoid in the heat and healthier alternatives

2026-06-27 17:28:52

Coast 2026: Amidst price chaos and security alarm

2026-06-27 17:07:55

Malta seizes food shipment from Albania: No documents and no temperature control

2026-06-27 16:51:59

The teller and the monologuer

2026-06-27 16:17:23

July ends with temperatures up to 40°C, what does July bring?

2026-06-27 15:38:37

Berisha: I am against towers, I did not sign any when I was prime minister

2026-06-27 14:31:10

When will he go to the US? How did Berisha respond?

2026-06-27 13:26:59

Berisha: Rama met with Ahmadinejad several times in Iran! He should resign!

2026-06-27 12:43:33

Who paid Chris Precht for the Prime Minister's private garden?

2026-06-27 12:29:02

Italian MEP comes to Tirana, joins the “Flamingo Revolution”

2026-06-27 11:04:24